Navigating KiwiSaver Fluctuations with Confidence

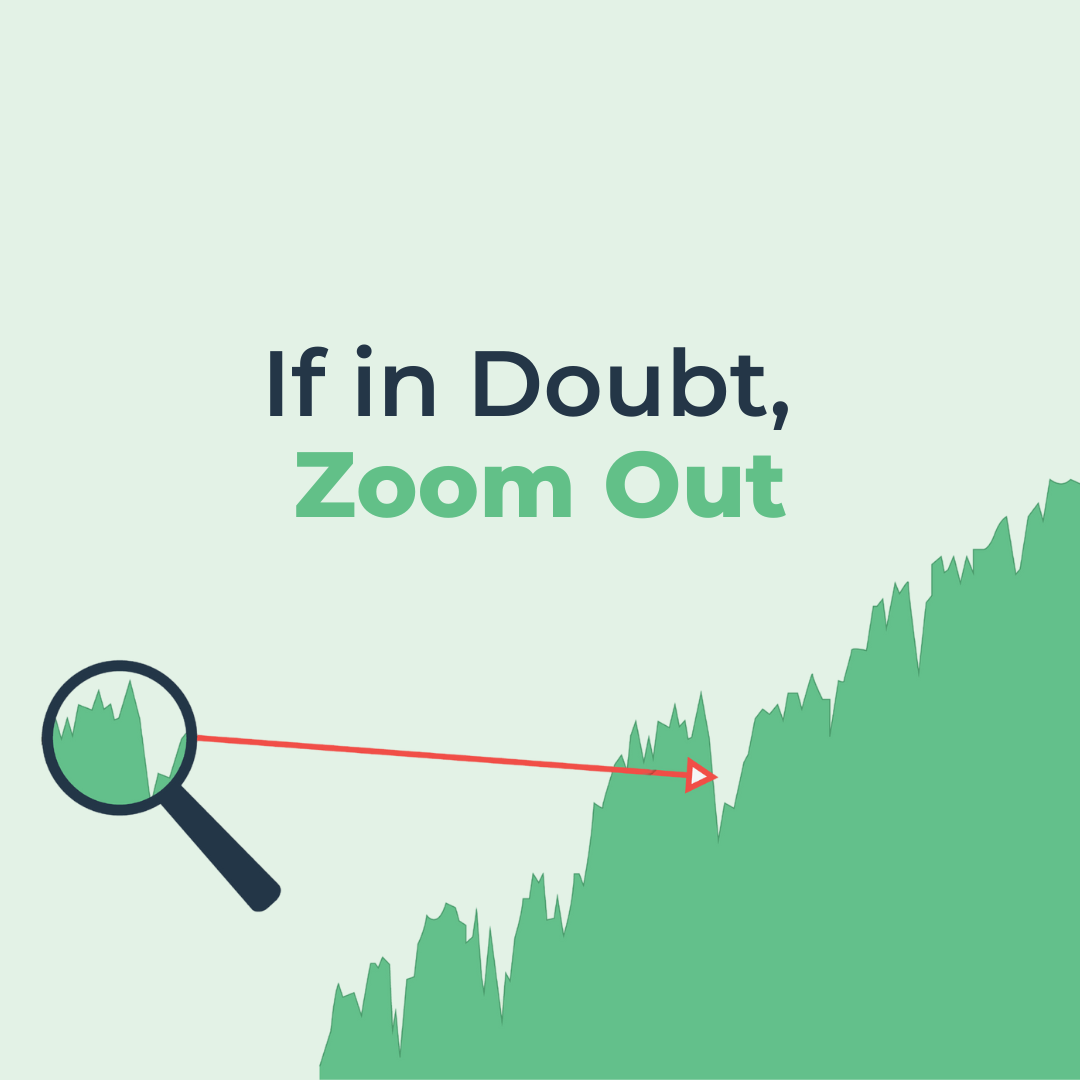

Ever opened your KiwiSaver account to see a dip in your balance and become stressed if you are in the right fund? It’s totally natural. But here’s a phrase to keep in mind for next time: “If in doubt, zoom out.”

Keep the Bigger Picture in Mind

Markets will go up and down—it’s just part of the process. The trick is to not lose sleep over the daily or even monthly swings. When you “zoom out” and look at the bigger picture, you’ll notice that those ups and downs tend to balance out over time. Sure, short-term dips can feel unsettling, but they’re typically just a small bump on the overall upward trend. Instead of focusing on short-term, try stepping back and looking at the bigger picture. Over the long term, your KiwiSaver will likely show a steady trend of growth, even if the road gets a little bumpy along the way.

Understanding Timeframes and Risk

Choosing the right KiwiSaver fund type is important, as you will need to ensure it aligns with your investment timeframe and the potential fluctuations you are willing to see. Every fund, from conservative to aggressive, will have a suggested timeframe of investment, that reflects its level of risk. If you’re planning to leave your funds invested for a longer period, a higher-risk, growth-focused fund might make sense. Yes, you’ll experience bigger fluctuations, but the potential rewards over time could be worth it. On the other hand, if you’re closer to needing your funds, a lower-risk fund will offer more stability and may be suited to protect against any unwanted fluctuations. Ensuring your fund matches your timeframe is key to staying confident in your KiwiSaver strategy and making the most of your investment.

Don’t Fall for the Doom and Gloom

There’s always someone predicting the next market crash. While these warnings can sound convincing, trying to “time the market” and jump in and out at the right moments is a risky game. The truth is, staying invested for the long term—time in the market—beats trying to perfectly time your moves. It’s the power of compound growth that works in your favour when you give your investments time to grow.

Final Thought

The market will always experience ups and downs, so it’s important that your KiwiSaver fund is aligned with your financial goals and timeframe. This ensures that the next time you log in and see a drop, you can confidently remember “if in doubt, zoom out”—knowing your fund is well-suited to your long-term strategy. Take a moment to reflect: does your current fund match your goals and timeframes? Whether you’re riding out fluctuations or considering adjustments, being in the right fund will make all the difference.